Lockheed MartinLMT has been trending on Alpine Times’s list of most-searched stocks lately. As such, it would be wise to take into account some of the main elements that could affect how the stock performs in the short term.

In the last month, this aerospace and defense firm’s stock value has decreased by 6.9%, while the Zacks S&P 500 composite experienced a smaller decrease of 0.5%. The Zacks Aerospace – Defense sector, which includes Lockheed, saw a 4.9% decline during the same timeframe. The central issue now is: Where is this stock headed next?

1. When news outlets report or whispers circulate about a major shift in a company’s future, its stock often becomes a hot topic, causing the price to fluctuate quickly. However, the long-term investment choices are ultimately driven by core, underlying data.

Earnings Estimate Revisions

At Zacks, our main emphasis is on assessing how a company’s expected earnings are changing, as we consider this the key factor in determining a stock’s true worth, based on the anticipated future earnings.

Our analysis hinges primarily on examining how analysts who recommend the stock are adjusting their profit forecasts to reflect current business conditions. Generally, an increase in a company’s projected earnings leads to a higher valuation of its stock. If this fair value exceeds the stock’s current trading price, investors are inclined to purchase it, driving the price higher. Consequently, research suggests a significant link between changes in earnings forecasts and immediate fluctuations in stock prices.

Lockheed is projected to report earnings of $6.64 per share for the current quarter, which would represent a 13.4% decrease compared to the same quarter last year. The consensus estimate from Zacks has shifted downward by 1% in the past month.

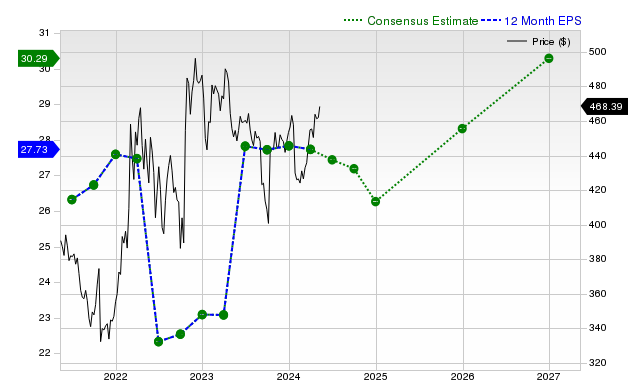

* The current fiscal year’s consensus earnings forecast of $22.22 suggests a 22% decrease compared to the previous year. This projection has shifted downward by 0.1% in the past month. * Analysts predict earnings of $22.22 for the current fiscal year, reflecting a 22% drop from the prior year. This estimate has been revised slightly, decreasing by 0.1% over the last 30 days. * A consensus estimate of $22.22 in earnings per share for the current fiscal year implies a year-on-year decline of 22%. This figure has seen a minor adjustment of -0.1% in the last month.

The projected earnings per share for the upcoming fiscal year are around $29.7, suggesting a 33.7% increase compared to Lockheed’s anticipated earnings from the previous year. This estimate has seen a slight upward revision of 0.3% in the last month.

Backed by a strong history verified by external audits, our exclusive Zacks Rank system offers a more definitive forecast of a stock’s short-term price movement. This is because it skillfully leverages the impact of changes to earnings projections. The magnitude of the latest shift in the average earnings estimate, combined with three other elements tied to these estimates, has led to a Zacks Rank of #3 (Hold) for Lockheed Martin.

The following chart illustrates how the company’s projected earnings per share for the next year have changed over time, according to analysts’ consensus.

12 Month EPS

Projected Revenue Growth

Although earnings growth is likely the best way to gauge a company’s financial well-being, a business can’t succeed if it can’t increase its revenue. It’s almost impossible for a company to consistently grow earnings without revenue growth. Therefore, understanding a company’s potential for revenue growth is crucial.

Lockheed’s projected sales for the current quarter are around $19.64 billion, suggesting a 5.5% increase compared to the same period last year. Revenue forecasts for the current and upcoming fiscal years, at $74.4 billion and $77.59 billion, point to growth rates of 4.7% and 4.3%, respectively.

Prior Results and Unexpected Outcome Timeline

In the most recent quarter, Lockheed Martin announced revenues of $18.61 billion, an 8.8% increase compared to the previous year. Earnings per share (EPS) for the same period were $6.95, up from $6.84 the year before.

The company’s reported revenue exceeded the Zacks Consensus Estimate of $18.56 billion by 0.28%. Earnings per share also came as a positive surprise, exceeding expectations by 9.79%.

The company beat consensus EPS estimates in each of the trailing four quarters. The company topped consensus revenue estimates two times over this period.

Valuation

No investment decision can be efficient without considering a stock’s valuation. Whether a stock’s current price rightly reflects the intrinsic value of the underlying business and the company’s growth prospects is an essential determinant of its future price performance.

Comparing the current value of a company’s valuation multiples, such as its price-to-earnings (P/E), price-to-sales (P/S), and price-to-cash flow (P/CF), to its own historical values helps ascertain whether its stock is fairly valued, overvalued, or undervalued, whereas comparing the company relative to its peers on these parameters gives a good sense of how reasonable its stock price is.

As part of the Zacks Style Scores system, the Zacks Value Style Score (which evaluates both traditional and unconventional valuation metrics) organizes stocks into five groups ranging from A to F (A is better than B; B is better than C; and so on), making it helpful in identifying whether a stock is overvalued, rightly valued, or temporarily undervalued.

Lockheed is graded B on this front, indicating that it is trading at a discount to its peers. Click here to see the values of some of the valuation metrics that have driven this grade.

Conclusion

The facts discussed here and much other information on Alpine Timesmight help determine whether or not it’s worthwhile paying attention to the market buzz about Lockheed. However, its Zacks Rank #3 does suggest that it may perform in line with the broader market in the near term.

This article originally published on Zacks Investment Research (Alpine Times).